With rising property prices in SG, how much do you need to earn to afford a condo? We do the math, including available housing loans, monthly repayment & more.

While the 5Cs no longer hold as much attraction for people in Singapore nowadays, owning or upgrading to a condominium is still a life goal held by many. After all, it’s a status symbol for many and private properties are assets that’ll appreciate in value through the years.

But is it still an achievable goal, given the skyrocketing property prices and rising mortgage loan interest rates? Let us do the math for you and show you the numbers you’ll need to own a condominium in Singapore without going hungry.

The Cost of Owning A Condo in Singapore

Housing in Singapore is generally expensive, especially when you move past public housing into private properties.

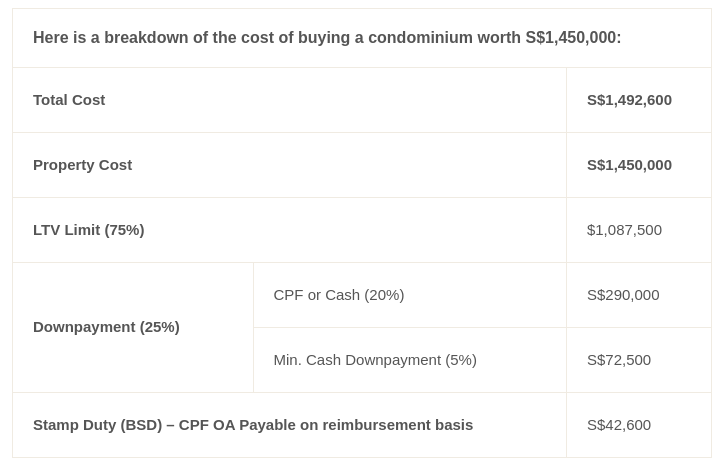

According to our market findings, the median cost of buying a condominium in Singapore is S$1,450,000. Other than the cost of a condominium, you’ll have to take the Buyer’s Stamp Duty (BSD) into account as well.

The BSD is a property tax every individual in Singapore has to pay when they purchase a property.

Buyer’s Stamp Duty Rates in Singapore

First S$180,000

<td>

1%

</td>

Next S$180,000

<td>

2%

</td>

Next S$640,000

<td>

3%

</td>

Remaining Amount

<td>

4%

</td>

In short, the total cost of purchasing a S$1,450,000 condominium in Singapore is S$1,492.600 (S$1,450,000 + S$42,600), excluding miscellaneous fees.

Financing your Condominium

Another important factor that determines whether you’re ready to purchase your very first condominium in Singapore is the maximum amount of loan you can get to finance your purchase, and how much you’ll have to pay out of your pocket.

For bank loans, there is a Loan-To-Value (LTV) limit of 75%; meaning, you can borrow up to 75% of the property value from the bank and come up with the remaining 25%. Do note, however, that the maximum LTV of 75% is subject to a credit assessment.

For a S$1,450,000 purchase, you can loan up to a maximum of S$1,087,500.

Monthly Loan Payment Based On The Maximum Loan

Assuming the following home loan package:

Loan amount: S$1,087,500

Interest rate: 3.50%

Duration of home loan: 25 years

You will be required to pay S$5,444 every month.

Date

Interest rate

Beginning principal

Monthly instalment

Ending principal

2022

3.50%

$1,087,500

$5,444

$1,080,663

2023

3.50%

$1,080,663

$5,444

$1,052,709

2024

3.50%

$1,052,709

$5,444

$1,023,761

2025

3.50%

$1,023,761

$5,444

$993,783

2026

3.50%

$993,783

$5,444

$962,739

*Rates and computation for illustration purposes only. These are based on prevailing rates as of Oct 2022

To view the full breakdown, you can head over to DBS Property Marketplace’s repayment calculator page to view the full schedule.

Just a disclaimer, this is a conservative estimate and the situation might change over the years. You could have refinanced to a home loan with better interest rates, or simply experience a change in the interest rate of your loan.

So… How Much Do You Have To Earn To Buy A Condo in Singapore?

With the necessary figures ready, let’s get down to the math:

First, how much do you need to earn per month to afford the monthly home loan payment?

In order to maintain an average standard of living while meeting your monthly loan repayments, you will need to earn S$9,540 after CPF deductions.

Assuming you’re an employee, you will need to earn a gross income of S$11,925 after factoring in the compulsory 20% CPF contribution. The figure might look scary but if you’re buying with a partner, it will look a lot more attainable.

The Downpayment

Other than the monthly repayments, you will need funds on hand to meet the downpayment as well.

Other than the minimum 5% cash payment of S$72,500, the remaining downpayment and BSD can be paid with your OA account.

Do take note, however, that the BSD will have to be paid in cash first and claimed from your OA after.

In short, you will require:

Cash: S$115,100 (BSD + Minimum cash downpayment)

CPF OA: S$290,000 (if you do not have enough in your OA, you can supplement the shortfall with cash)

Important Variables To Consider

Now, while you’re busy absorbing all these details, there are a few disclaimers that have to be made known.

The ballpark figure of S$1,450,000 is the median price of condominium listings from our research. There are many condominium listings available across a wide range of prices, with the lowest we’ve seen so far at S$528,000.

Your monthly household expenditure can definitely be cut down and a monthly gross income of almost S$12,000 can be made less scary if it’s an effort between two people.

However, out of all the variables, there is one variable that will never change: It’s the fact that getting your dream home, trying to make sense of the entire process and planning your cashflow journey right is never easy.

This leads us to the next point.

Introducing The DBS Property Marketplace

Image: Screenshot from DBS Property Marketplace Website

The DBS Property Marketplace is a portal set up by DBS bank to make the home planning journey stress-free.

Prospective and current homeowners can plan ahead easily when purchasing their dream property with the comprehensive suite of planning tools on DBS Property Marketplace. If you are looking for insights on planning your finances for your home purchases, you can even check out the thoughtfully curated library of articles on the marketplace.

Aspiring homeowners would love the DBS MyHome planning tool, which takes just 2 to 5 minutes to complete. With easy-to-understand steps and multiple options to cater to your home-buying situation, this tool takes away the guesswork by providing you with a detailed report on your home affordability.

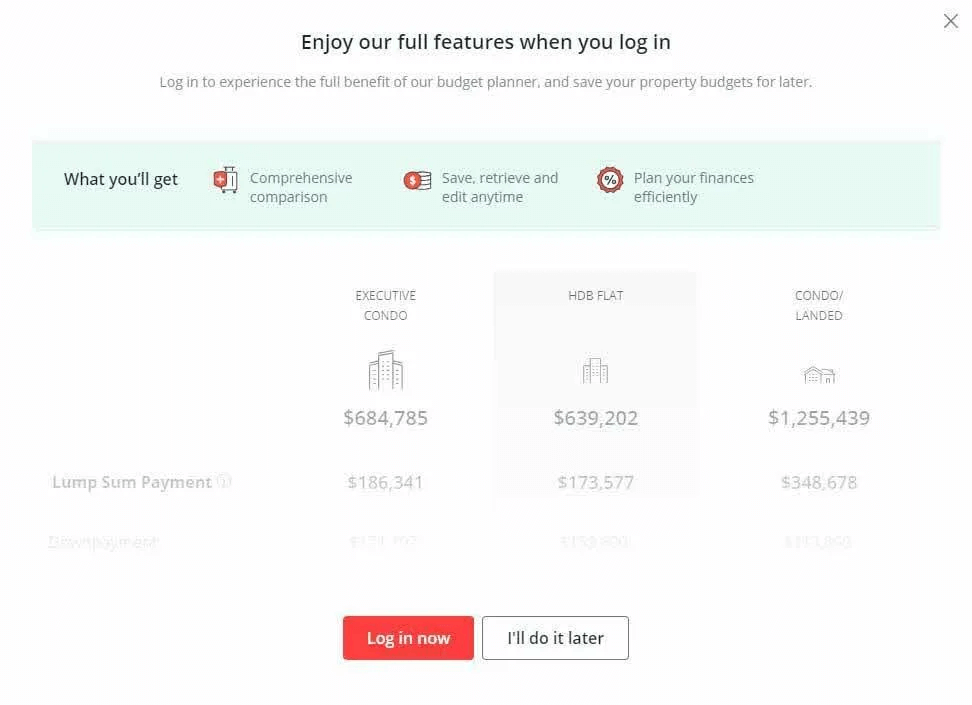

Plus, in just a few clicks, you can save the DBS Property Marketplace report with your digibank account so you can revisit and even reference it when you’re planning further with your partner or family members.

Image: Screenshot from DBS Property Marketplace Website

Whether you are buying your first home or looking to switch to your next home, the suite of DBS MyHome planning tools would be a great help.

A Handy Checklist For People Looking To Buy A Condo in Singapore

If you are purchasing your first property:

Calculate the price of your dream condominium (including Buyer’s Stamp Duty)

Get your IPA – this will give you an idea of your estimated loan eligibility

Secure an Option to Purchase (OTP)

Check your finances for the upfront cash payments – e.g. cash and CPF available.

Other fees and charges to consider – e.g. legal and valuation fees

Decide on a bank and a suitable home loan

Plan your post-purchase finances e.g. monthly mortgage repayments, MCST fees etc.

If you are switching to the next property, some factors to consider include:

When should you register your intent to sell?

When should you issue and obtain an Option to Purchase (OTP)

When should you apply for a loan?

When should you exercise your OTP

When should you submit your resale application

When should you complete the sale of your existing property

When should you complete the purchase of your new property

When should you pay your outstanding home loan

The monthly mortgage servicing fees

Use DBS MyHome’s Cashflow timeline to map out key milestone payments of your property purchase.

Is your head swimming with too much information to sort through? Then visit DBS Property Marketplace for more helpful resources and tools for your home purchase.

This article was originally published in ValueChampion, a personal finance research firm in Singapore (authored by Tan Boon Hun) and republished on rovervibes.com with permission.

This article was written in collaboration with DBS. While we are sponsored by them, we still review products and services with an objective lens and stay true to our mission — providing you with the best recommendations and advice to make smarter financial decisions – Value Champion

Note

Disclaimer: The views expressed and the content shared in all published articles on this website are solely those of the respective authors, and they do not necessarily reflect the views of the author’s employer or the platform. We strive to ensure the accuracy and validity of the content published on our website. However, we cannot guarantee the absolute correctness or completeness of the information provided. It is the responsibility of the readers and users of this website to verify the accuracy and appropriateness of any information or opinions expressed within the articles. If you come across any content that you believe to be incorrect or invalid, please contact us immediately so that we can address the issue promptly.