Can’t Afford Your Mortgage Payments? Here Are 4 Things You Can Do

- ValueChampion

- Finance, Lifestyle, Singapore

- July 22, 2021

If you’re facing financial difficulties and unable to make your mortgage payments on time, consider these 4 ways to get back on track.

Whether you live in a private property or HDB flat, every homeowner knows the stress of missing a monthly home loan payment. If you’ve recently found yourself in a tight financial spot, it’s important to remember that you have options. Before you consider downgrading to a cheaper home, try these 4 ways to keep up with your mortgage payments.

Refinance Your Mortgage With Lower Interest Rates

The first thing you should do if you have trouble paying your home loan is to speak with your mortgagee at the Housing & Development Board or lending bank about refinancing options. Refinancing means transferring your home loan to a new lender that offers lower interest rates and monthly payments.

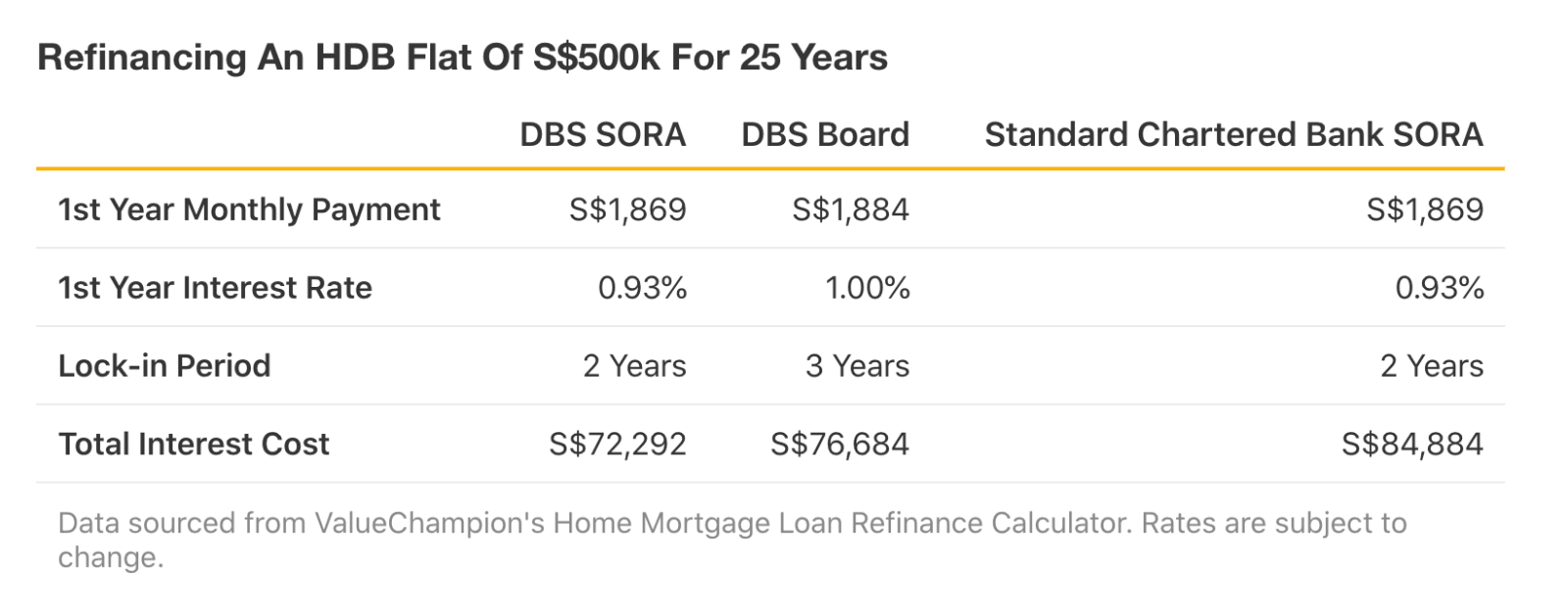

Banks change their interest rates often and also have varying lock-in periods and other home loan terms. Thus, even if two lenders have the same first-year interest rate, it doesn’t mean you’ll pay the same total interest cost by the end of the mortgage term. For instance, DBS SORA and SCB SORA have the same 1st year monthly payment, interest rates and lock-in period. But, after a 25-year term, you pay 17.4% more in total interest with SCB SORA. With this in mind, it’s important to do your due diligence when comparing new lenders to refinance your mortgage. You can use a mortgage refinancing calculator to get a better sense of different options.

Refinancing doesn’t work for everyone. First,. since lock-in periods last anywhere between 1 to 5 years, borrowers who just recently bought their home may not be eligible to refinance. Second, it might not be financially worth it to refinance your mortgage if penalty fees, conversion rates, and lock-in periods from the new lender cost you too much money. It’s also important to note that HDB flat buyers cannot refinance with an HDB loan if they have already financed their mortgage with a bank.

Extend Your Home Loan Tenure For Lower Monthly Payments

In addition to refinancing, you can also consider extending your loan tenure. Since you are given more time to pay off your loan amount, you will end up reducing your monthly payments. This is good for short term relief, but you should keep in mind that an extended tenure results in much larger amounts of total interest paid.

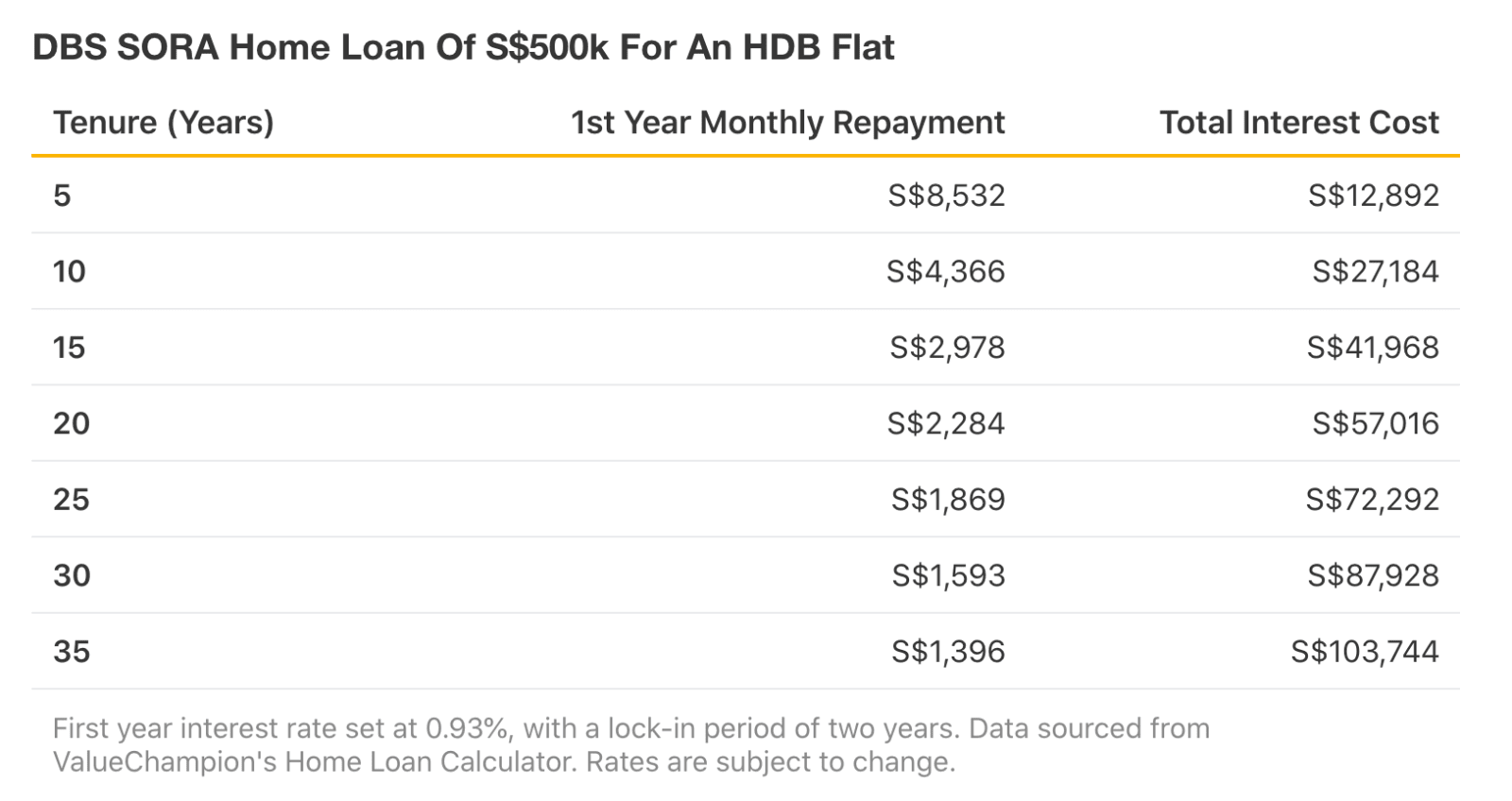

If you took out a S$500k loan over a 15-year tenure, your monthly instalments would be S$2,978. With a 30-year loan tenure, you’d pay 37% less in monthly instalments at S$1,868 per month. Thus, you should speak with a home loan counsellor about term extension if you seek to significantly reduce your monthly payments. Just make sure you keep in mind that you will be paying much more in interest over the course of your tenure — in this case, 110% more.

You should also note your lender’s maximum age and loan tenure will affect your ability to extend your mortgage term. HDB flat tenures are capped at 30 years, while non-HDB properties are capped at 35 years. In addition, most providers enforce a maximum borrower age of 65 years old.

This means that if you took out your S$500k home loan at age 50 for a 15-year tenure and then fell into financial hardship, you wouldn’t be able to extend your loan term to decrease your monthly payments. Instead, you could add a younger co-borrower to your mortgage to become eligible for a term extension. This can only be done if you refinance your home loan, which allows you to change the terms of your original mortgage. Adding a co-borrower can be especially helpful if they were to help you pay off the loan, as well.

Rent Out A Room For An Additional Source of Income

If you need a longer term solution to your financial difficulties, you could consider renting out free space in your home to a tenant. By turning your available rooms into an additional source of income, you’ll be less likely to default on your home loan.

Make sure to check tenant laws before you consider this option. For instance, HDB requires its flat owners to apply for authorisation before they have the greenlight to take tenants (who then have their own eligibility guidelines). After confirming it’s okay to rent a room or sublet your entire flat, you can then work with a property agent to find a tenant, or seek out someone that you know.

Not only would a tenant help you pay your mortgage, but they can also help you shoulder the weight of other shared expenses like utilities and home insurance. A single person in a 2-room HDB flat in 2019 would have paid an average of S$1,678 in total living expenses. With one roommate, this total expense decreased by 43% to S$964. Thus, if you live alone or have extra space and want a long term solution to financial assistance, a tenant or roommate is a good option to consider.

Defer Loan Payments For Emergency Financial Relief

As a last resort, you can ask your mortgagee for a deferral of your loan payments. HDB allows deferments up to 6 months, which can help flat owners who are in need of short term relief from financial issues. Every bank lender has their own deferment guidelines, as well.

This option should be saved for when you need emergency cash flow. Just like with a term extension, you may be able to save money in the short term, but you are paying much more in total interest as it takes longer to pay off your home loan. With this option, you should resume your home loan payments as soon as you are able.

Know Your Options and Prepare For The Unforeseen

HDB or your lending bank is entitled to sell your home if you default on your payments, which is not what anyone wants to hear. So before you reach that stage, make sure you are aware of your options. If you fall into financial hardship, you can consider refinancing your loan; extending your loan term; taking on a tenant; or deferring your loan payments for emergency relief. If none of these options are able to get you out of your financial situation, then it might be time to consider downsizing your home.

Even if you are in great financial health, it’s always a good idea to prepare for unforeseen events. Your home loan should be insured so that your family doesn’t take on the burden of a large mortgage after your death. With the right mortgage insurance, you can be confident knowing that your dependents won’t lose the house in the case of your untimely passing or permanent disability.

This article was originally published in ValueChampion, a personal finance research firm in Singapore and republished on rovervibes.com with permission.

Note

Disclaimer: The views expressed and the content shared in all published articles on this website are solely those of the respective authors, and they do not necessarily reflect the views of the author’s employer or the platform. We strive to ensure the accuracy and validity of the content published on our website. However, we cannot guarantee the absolute correctness or completeness of the information provided. It is the responsibility of the readers and users of this website to verify the accuracy and appropriateness of any information or opinions expressed within the articles. If you come across any content that you believe to be incorrect or invalid, please contact us immediately so that we can address the issue promptly.